Buying Short Sales: What You Need to Know

As the real estate market remains volatile, one of the best options for many new homebuyers is purchasing a short sale home. But, what does "short sale" mean? A short sale is when lenders have the opportunity to sell a property before the bank forecloses on the home rather than after. While buying short sales creates the opportunity for real estate investors to pay well-below-average housing prices for properties within ideal locations, there are still drawbacks.

If you're interested in buying short sales, here are a few things you need to be aware of:

Why Banks Short Sale Pre-Foreclosure Homes

The last thing a bank wants to do is own a property secured by the bank's loans. When a property owner is in default and owes more than what the home is currently worth, the bank will work with the seller to offer the property for less than they owe on the mortgage loan.

How much money will banks take off? When buying short sales, how much should I expect prices to fluctuate? On average, banks estimate that holding on to the property after foreclosure will cost up to 18 percent of the home value to complete the inspection, appraisals, repair and maintenance. Instead, it is a much easier and financially sound decision for banks to sell the home "as is" to avoid any third-party inspection process.

What to Consider Before Buying a Short Sale

Buying short sales might seem like a good deal for the buyer, but that's not always the case. Here are three major conflicts buyers and sellers face when a short sale, pre-foreclosed home is on the market:

Time: Don't let the name fool you. Buying short sales takes a very long time. There's a whole gambit of scenarios of why a short sale might be delayed, but many of the hurdles buyers have to overcome have to deal with secondary financing on the homeowner's original mortgage, bank processing delays and private mortgage insurance policy breakdowns. Buying short sales is a very complex process, which can leave the short sell buyer in housing limbo for up to six months.

Condition: Short sale homes often need additional maintenance and repairs. When the current property owner is unable to pay the mortgage on the home, more often than not the condition of the property diminishes over time. Additionally, short sale homebuyers should take into account that the property will have had more than one previous owner, which adds to the wear and tear.

Lender Restrictions: Banks can renegotiate a short sale at the last second. If a new law passes, the market begins to change or the bank finds out more information about the property, they reserve the right to change the terms of the contract at any point in the process. Banks will also refuse to pay for extra services like seller closing costs or inspections. If you want something specific inspected on the property, you're probably going to pay for it yourself.

Short sale homes are the real estate market's diamond in the rough. It's true that buying short sales can be a very tricky process, but for the flexible and patient homebuyer, the short sale home can be the dream house they've been searching for.

Wednesday, December 14, 2011

Tuesday, December 13, 2011

How to Avoid Rental Scams

You find yourself in the market to find a new place to rent, and you are searching through Craigslist to find your next place. Craigslist is a great place to search but be forewarned, there are many unscrupulous people out there ready to take your money.

There are a number of fake rental scams on Craigslist and other classifieds. People are out to steal your money so here are some tips from the Better Business Bureau on how to avoid these scams.

The email addresses they use usually are from yahoo, ymail, rocketmail, fastermail, live, hotmail and gmail, and they also post ads under anonymous craigslist addresses. They frequently change their aliases. Some things to watch for:

There are a number of fake rental scams on Craigslist and other classifieds. People are out to steal your money so here are some tips from the Better Business Bureau on how to avoid these scams.

The email addresses they use usually are from yahoo, ymail, rocketmail, fastermail, live, hotmail and gmail, and they also post ads under anonymous craigslist addresses. They frequently change their aliases. Some things to watch for:

- The deal sounds too good to be true. Scammers will often list a rental for a very low price to lure in victims. Find out how comparable listings are priced, and if the rental comes in suspiciously low, walk away.

- They use photos stolen from other property advertisements or from home furnishing catalogs or hotel websites.

- They use fake names, often stolen from Facebook profiles or networking sites. Often they assume the identities of previous victims.

- What they all have in common is that sooner or later you get a request to transfer funds via Western Union, Moneygram or some other wire service.

- Never under any circumstances, wire money at the request of any prospective “landlord” via Western Union, Money Gram or any other wire service. Even if they tell you to wire the funds to a friend or relative’s name “to be safe,” it’s a trap!

- Never send a scan of your passport or other ID. These thieves will use your identity to scam others. Ask to see the landlord's ID - record all the information you can from it.

- Use a browser to search for the person's name who you're dealing with. Be sure to add quotes around their name. You could add the words "fraud" or "scam" at the end of your search terms.

- Use reverse directory look up if the person has given you their telephone number. It's important to double check that they are who they say they are.

- Visit the local county courthouse to look up property ownership for the property in question. Who really owns it? Is it the person you're dealing with? Or someone else?

- Scan any provided photographs carefully. Do they match up with what you've seen in person? Do they look like they all came from the same place?

- They don't ask for an application or permission to check your credit? That's a red flag!

- Considering the current state of our economy and the rise in foreclosures, ask the landlord if they're current on their mortgage payments, and then get their answer in writing.

- Consider using another method for obtaining a rental, i.e. real estate agent, going through a rental agency, etc.

- Always check bbb.org to see if the “company” has any complaints.

Tuesday, December 6, 2011

New Wal-Mart Coming to Cedar Park

Retail giant Wal-Mart expects to build another store in Cedar Park on the northwest corner of RM 1431 and Ronald Reagan Blvd.

The 150,000-square-foot store will employ about 300 associates, said Kellie Duhr, director of public affairs and government relations for Wal-Mart.

Wal-Mart has not announced construction dates or a timeline for opening the store, she said. Cedar Park Director of Economic Development Phil Brewer said he is excited Wal-Mart chose Cedar Park as the site for another store.

“It obviously is an economic impact from a tax standpoint, from ad valorem and sales taxes generated,” he said. “Typically your big box stores like this are going to produce something like $80-$100 million in total taxable sales.

The 150,000-square-foot store will employ about 300 associates, said Kellie Duhr, director of public affairs and government relations for Wal-Mart.

Wal-Mart has not announced construction dates or a timeline for opening the store, she said. Cedar Park Director of Economic Development Phil Brewer said he is excited Wal-Mart chose Cedar Park as the site for another store.

“It obviously is an economic impact from a tax standpoint, from ad valorem and sales taxes generated,” he said. “Typically your big box stores like this are going to produce something like $80-$100 million in total taxable sales.

Wednesday, November 30, 2011

Home Buying Tips: Negotiating House Price

Making an of Offer on a House Without a Buyer's Agent.

Thinking about making an offer on a house without a real estate agent? Nervous about negotiating the best house price in this crazy economy? We don't blame you. When it comes to buying a home, negotiation can mean the difference between a few thousand dollars and tens of thousands of dollars. It's stressful and scary, especially if you're doing it without an experienced real estate agent. Negotiating a home selling contract in this current real estate market is also financially tricky. This is where an experienced agent who has sold in times of real estate booms and past real estate slumps can save you more than the commission you pay them.

For those brave enough to consider making an offer without a buyer's agent, here are a few tips on negotiating house price:

Negotiating House Price Tip #1: Arm Yourself with Information

The most important information is a Comparable Market Analysis (CMA), which is a neighborhood survey of the similar and recently sold homes in your neighborhood of choice. There are several places you can get partial information about sold houses online these days, but it is important to choose the right homes and get full information. This is another way a professional real estate agent can help you save money. Agents have access to the most up-to-date real estate data and are experts at figuring out which houses truly belong in a CMA. More importantly for today's economy, a real estate agent can tell you how short sales and foreclosures in the neighborhood can affect negotiating an offer. House pricing is very tricky in this economy.

Once you have access to a detailed CMA, check out the houses as much as possible. A real estate agent might be able to get inside some of the houses that were just recently sold or have a current offer. You can check to see if the house you're looking at is up to par or if it falls frighteningly below the homes listed in the CMA. This is a great way to tell if your house is near the proper price point or if there is leeway in negotiating an offer. House pricing is much more complicated these days than it used to be. Rather than comparing features like which houses have pools and which don't, buyers are weighing short sales against foreclosures and traditional home sales.

Negotiating House Price Tip #2: Figure Out the Seller's Motivation

Information is key in negotiating house price. But, finding out how your dream house price compares to the market is only part of the process. The second is figuring out the seller's motivation. It's the fun part of play detective and look inside the home seller's mind for a minute. Do they have to sell their house or do they want to sell? Motivation isn't always revealed and the seller's agent doesn't necessarily have to give you this information. However, if you have a good real estate agent, he or she often can get the information from the seller's agent.

Have too reasons:

- They are relocating for a job.

- They just got laid off and can't afford the mortgage.

- The house is close to foreclosure and they don't want to ruin their credit history.

- They just had an addition to their family and truly don't have enough space.

- They are testing the market to see if they could sell their house.

- They want to buy a different house while housing prices are down.

- They want to buy a new house while mortgage rates are low.

Negotiating House Price Tip #3: Don't Waste Time

Buying a home can be super stressful. You don't have time to waste with sellers who won't budge and you shouldn't waste the seller's time with a low-ball offer.

How do you know if sellers are wasting your time? If they won't discuss asking price in relation to similar homes in the neighborhood, they probably are not serious about selling the home. Sellers will do this when they're unsure about moving or to figure out how much they can get for their property.

Just as they shouldn't waste your time, don't waste theirs. Don't give them a low-ball offer just to see if they bite. It makes you seem like you're not ready to buy or that you want to scam them. If you are truly interested in the house, this is not a good negotiating tactic.

Negotiation is an art, not an exact science. Experienced real estate agents have practiced different techniques and know what works when negotiating house price and what doesn't. Once again, in today's economy, negotiating house price can be much easier if you have an experienced agent on your side. Negotiating a home selling contract is a tricky proposition if done on your own.

Monday, November 28, 2011

HUD Home Sales Incentives

HUD is offering several new sales incentives on HUD homes that will

make these homes more affordable for homebuyers. The incentives vary

from state to state, but may include the following:

- $100 down payments on HUD Homes financed with FHA-insured financing

- Sales allowances that can be used to pay closing costs, make repairs, or pay down the mortgage amount

- Broker bonuses for owner-occupant sales.

Monday, November 21, 2011

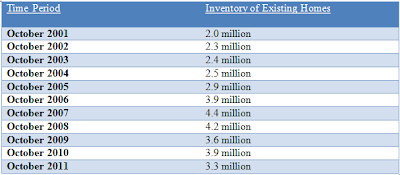

Lowest Inventory in Six Years

The total homes listed for sale continue to move downward. The latest decline in October to 3.33 million was partly seasonal, as autumn and winter months nearly always have fewer listings in comparison with spring and summer months. Still, examining listings only in the month of October (so as to get an apple-to-apple comparison), this year saw the lowest inventory since 2005.

A review of June, July, August, and September data also says the same thing: namely, 2011 had the lowest inventory count since 2005 across same-month comparisons. The market is clearly healing and the falling inventory is an early indicator as to what will happen to home prices in the future.

A review of June, July, August, and September data also says the same thing: namely, 2011 had the lowest inventory count since 2005 across same-month comparisons. The market is clearly healing and the falling inventory is an early indicator as to what will happen to home prices in the future.

Despite the improving inventory trend, let’s be mindful that the current inventory conditions are still considered elevated and above normal compared to the early years of the last decade. Also the months-supply – i.e., how many months it would take to exhaust the current inventory assuming the current sales pace – stood at 8 months in October, which is still a tad above normal conditions. Ideally, the months-supply figure needs to fall to about 6 months before prices show consistent positive movement of about 3 to 5 percent annually.

Separately, the inventory of newly constructed homes (not existing home inventory) is at 40 year lows because homebuilders have just not been able to break ground and build new homes because of very difficult lending conditions in obtaining construction loans. The inventory trends for both existing and new homes should therefore provide some reassurance that home price growth (at the national level) could be just around the corner. Local markets in Bismarck, Buffalo, Pittsburgh, San Diego, and Washington, D.C., as some examples, have already shown consistent price gains.

Source - National Association of Realtors - Economic Outlook 11-12-2011

Despite the improving inventory trend, let’s be mindful that the current inventory conditions are still considered elevated and above normal compared to the early years of the last decade. Also the months-supply – i.e., how many months it would take to exhaust the current inventory assuming the current sales pace – stood at 8 months in October, which is still a tad above normal conditions. Ideally, the months-supply figure needs to fall to about 6 months before prices show consistent positive movement of about 3 to 5 percent annually.

Separately, the inventory of newly constructed homes (not existing home inventory) is at 40 year lows because homebuilders have just not been able to break ground and build new homes because of very difficult lending conditions in obtaining construction loans. The inventory trends for both existing and new homes should therefore provide some reassurance that home price growth (at the national level) could be just around the corner. Local markets in Bismarck, Buffalo, Pittsburgh, San Diego, and Washington, D.C., as some examples, have already shown consistent price gains.

Source - National Association of Realtors - Economic Outlook 11-12-2011

Friday, November 11, 2011

Lender Delays & How to Avoid Them

So you’ve found your perfect home. The paperwork has all been signed, everyone is excited, and then you get the news. Your lender can’t process your mortgage loan application in the time you’ve allotted in the contract!

In a video put out by the Legal Department @ Texas Association of Realtors this is a real issue that concerns all parties to a real estate transaction.

As a buyer, when you are searching for a lender to assist you in purchasing your new home make sure you ask “What are your estimated turn times on the following: (1) Processing (2) Underwriting (3) Conditions (4) Closing Docs". Having accurate numbers is really important in a contract to purchase a home. If you put a short time- frame in the contract to secure financing, you may put yourself in a bad position. Example, if you place in your contract that you will be closing in 30 days but it takes your lender 45 days to secure financing on average. You may find yourself in breach of contract!

In a video put out by the Legal Department @ Texas Association of Realtors this is a real issue that concerns all parties to a real estate transaction.

As a buyer, when you are searching for a lender to assist you in purchasing your new home make sure you ask “What are your estimated turn times on the following: (1) Processing (2) Underwriting (3) Conditions (4) Closing Docs". Having accurate numbers is really important in a contract to purchase a home. If you put a short time- frame in the contract to secure financing, you may put yourself in a bad position. Example, if you place in your contract that you will be closing in 30 days but it takes your lender 45 days to secure financing on average. You may find yourself in breach of contract!

Wednesday, November 9, 2011

Steps in Home Buying Process: Pre-Approval for Home Loan

Here are some reasons why being approved at the beginning of the home buying process is so important:

Pre-approval is one of the most important steps in the home buying process. You should apply for a loan and receive approval from a lender before searching for a home.

- Pre-approval for a home loan will determine your price range. Based on your down payment and that pre-approved mortgage amount, you'll know what you can afford before you start looking. This saves you time and allows you to focus on houses that you can actually purchase.

- Pre-approval strengthens your offer and negotiating position. Home sellers tend to accept an offer from a buyer who is pre-approved for a home loan over someone whose financial picture is still in question.

- Pre-approval often cuts days or even weeks when you close. The lender has already analyzed your credit and approved you for a mortgage.

What is the difference between being pre-approved and pre-qualified?

What is the difference between being pre-approved and pre-qualified?

There is actually a big difference between buyers who are pre-qualified and those who are pre-approved. Lenders pre-qualify buyers and determine how much they can borrow based only on information the buyer has provided. The buyer still must fill out a loan application and go through the lender's approval process. If you are pre-approved, lenders have already done a credit check and verified employment and deposit. Pre-approval is a commitment to lend you a predetermined amount. The only piece missing is the lender's appraisal of the home to confirm its value.

How long should a pre-approval for home loan take?

If you are dealing with an experienced mortgage representative who uses an automated approval system, it should only take a few minutes to get a pre-approval. However, if your lender is not using the most up-to-date automated systems, pre-approval for a home loan could take a few days. The automated system takes all of your income, debt and asset information and enters it into their computer. The pre-approval process is usually pretty fast as long as the loan officer is certified to use the DU underwriting system (automated underwriting). The final loan approval comes once you have an actual property and then the lender re-verifies all of the property, income, debt and asset information.

What happens if I change jobs after getting pre-approval for a home loan? Do I have to go through the process again?

Unfortunately, the answer is usually yes. Your pre-approval is good as long as none of the information provided to the lender changes. You will need to notify the company that pre-approved you that your employment status has changed. They will have to enter your new income data. The good news is that if you took a new job that pays more, you might be able to afford a larger house.

What happens if I decide to work for myself after getting pre-approval for a home loan?

There will be complications when going from W-2 employee to 1099 or Schedule C income. You will probably need a two-year history of self-employment to qualify with that income. In this instance, you might want to ask your lender about undocumented home loans.

Subscribe to:

Posts (Atom)